Math recap: the Wiener process

A standard Wiener process on is a continuous-time stochastic process satisfying:- Independent increments: for , , independent of the path up to time

- Continuous paths

Brownian motion in motion

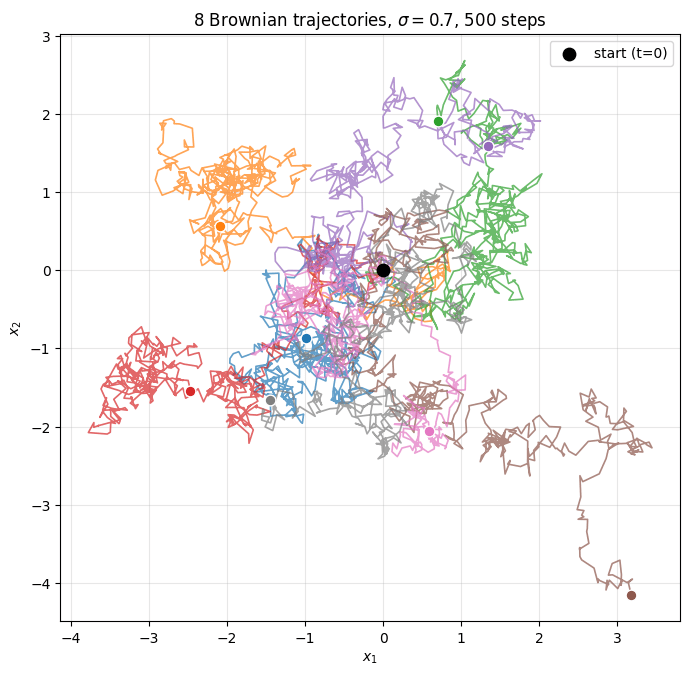

Eight particles released from the origin, each tracing an independent random walk. The trail behind each particle is its history, short trajectories on either side of the origin diverge into the wider variance the longer the chain runs.Eight Brownian trajectories

Eight particles released from the origin, each undergoing an independent random walk over 500 steps with and . The colored end-dots mark each trajectory’s final position; the black dot at the origin marks the common start.

Snapshot grid at the same timesteps as the DDPM forward process

200 fresh particles released from the origin, snapshotted at , the same timesteps the DDPM tutorial uses for its forward-noising visualization. The cloud spreads with variance proportional to , the hallmark of a Wiener process.

Connection back to diffusion

Continuous-time diffusion frames the forward process as the SDE where is exactly the Brownian motion above. The variance-preserving SDE used by DDPM picks and , so the marginal stays Gaussian and the variance is bounded. The discrete chain you trained earlier is the Euler-Maruyama discretization of this SDE. Two takeaways:- Forward = Brownian motion + drift. Everything diffusion-model-related sits on this foundation.

- Reverse = score-based ODE/SDE. Anderson’s reverse-time SDE is what your trained approximates; deterministic DDIM is the probability-flow ODE limit.

References

- Anderson. Reverse-time diffusion equation models. Stochastic Processes Appl. 1982.

- Song et al. Score-Based Generative Modeling through Stochastic Differential Equations. ICLR 2021. arxiv.org/abs/2011.13456

- Karatzas & Shreve. Brownian Motion and Stochastic Calculus. Springer 1991. (textbook)